The Visalia Times-Delta recently published an editorial of mine defending section 501(c)(4) organizations that have been vilified as of late as a reactionary response to the IRS tea party scandal. I defend both their tax-exempt status and the fact that donors' names are kept confidential.

Friday, June 28, 2013

Thursday, June 27, 2013

How the Prop 8 Ruling Threatens Prop 13 (and other future tax reforms)

California's ballot initiative process is vital to Californians and helps ensure that the will of the people is expressed, even when California politicians are uncooperative. Over the years, ballot initiatives have been proposed and passed that have advanced both liberal and conservative causes. In each of these cases, the initiative process was the only way to advance these issues as the legislature would not, or could not, pass effective legislation.

While the recent Supreme Court case on Proposition 8 may have advanced gay marriage, its unintended consequence is to put into question the sustainability and power of future ballot initiatives. Justice Scalia ruled, in essence, that the defenders of the Prop 8 initiative did not have standing to sue because only the State of California had standing to defend Prop 8 from attacks. While Gov. Brown and Kamala Harris, the State A.G., put up a begrudging defense of Prop 8 at the trial level, they opted not to appeal the trial court decision finding Prop 8 unconstitutional. Defenders of Prop 8 then stepped in and decided to appeal. The California Supreme Court held that clearly, the Prop 8 defenders had standing and could appeal the decision and were essentially representing the interests of the State.

Unfortunately, Justice Scalia's holding now weakens almost any ballot initiative--especially those that the Governor and Attorney General personally dislike. Consider the following hypothetical. A homeowner sues alleging that Prop 13 violates their equal protection because their neighbor who bought their home 50 years ago pays much less than they do for their new home, despite the fact the homes are identical and have the same value. Although merit less, the Governor and state AG could opt to not defend the suit. All of a sudden, an injunction is issued finding Prop 13 to be unconstitutional. The State decides it won't pursue an appeal and the defenders of Prop 13 have no standing in federal court to pursue an appeal either.

In a single opinion, Justice Scalia was able to do something many California politicians have been trying to do for year--weaken the initiative process.

While the recent Supreme Court case on Proposition 8 may have advanced gay marriage, its unintended consequence is to put into question the sustainability and power of future ballot initiatives. Justice Scalia ruled, in essence, that the defenders of the Prop 8 initiative did not have standing to sue because only the State of California had standing to defend Prop 8 from attacks. While Gov. Brown and Kamala Harris, the State A.G., put up a begrudging defense of Prop 8 at the trial level, they opted not to appeal the trial court decision finding Prop 8 unconstitutional. Defenders of Prop 8 then stepped in and decided to appeal. The California Supreme Court held that clearly, the Prop 8 defenders had standing and could appeal the decision and were essentially representing the interests of the State.

Unfortunately, Justice Scalia's holding now weakens almost any ballot initiative--especially those that the Governor and Attorney General personally dislike. Consider the following hypothetical. A homeowner sues alleging that Prop 13 violates their equal protection because their neighbor who bought their home 50 years ago pays much less than they do for their new home, despite the fact the homes are identical and have the same value. Although merit less, the Governor and state AG could opt to not defend the suit. All of a sudden, an injunction is issued finding Prop 13 to be unconstitutional. The State decides it won't pursue an appeal and the defenders of Prop 13 have no standing in federal court to pursue an appeal either.

In a single opinion, Justice Scalia was able to do something many California politicians have been trying to do for year--weaken the initiative process.

Monday, June 24, 2013

IRS Sent $7,319,518 in Refunds to a Sinlge Bank Account Used by 2,706 Aliens

According to a recent audit report by the Treasury Inspector General, the IRS sent $7,219,518 in tax refunds in 2011 to what where--at least on paper--2,706 different aliens who were not authorized to work inside the United States. Unbelievably, all the funds were deposited into a single account.

In terms of strengthening fraud and theft detection, you would think that stopping this type of obvious abuse would be the "low-hanging fruit".

In terms of strengthening fraud and theft detection, you would think that stopping this type of obvious abuse would be the "low-hanging fruit".

Thursday, June 20, 2013

IRS FBAR Tax Forms Due June 30

Chances are, if you immigrated to the U.S. or if you travel frequently abroad, you have a foreign bank account. However, what most don't know is that you must take active steps to notify the IRS of these foreign accounts even if they are not earning any income. Failure to do so can lead to massive penalties. In particular, the penalty for knowingly failing to file the requisite form is up to 50% of the total value of the account.

What must be filed is referred to as an FBAR, and it must be received by the IRS by June 30th. If you have failed to file FBARs in the past then there are ways to come into compliance at a minimal tax cost. Keep in mind that foreign banks are now repeatedly turning over U.S. account holder information to the DOJ and IRS and so the notion of a "secret" foreign account (Swiss or otherwise) is a thing of the past. If the IRS discovers the account before you come clean, it is likely that the penalties and interest will exceed the value in the account, even if absolutely no taxable income was earned by the account.

What must be filed is referred to as an FBAR, and it must be received by the IRS by June 30th. If you have failed to file FBARs in the past then there are ways to come into compliance at a minimal tax cost. Keep in mind that foreign banks are now repeatedly turning over U.S. account holder information to the DOJ and IRS and so the notion of a "secret" foreign account (Swiss or otherwise) is a thing of the past. If the IRS discovers the account before you come clean, it is likely that the penalties and interest will exceed the value in the account, even if absolutely no taxable income was earned by the account.

Tuesday, June 18, 2013

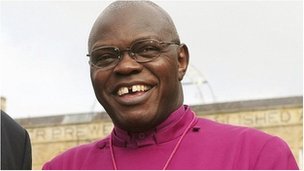

Tax Avoidance Sinful, Says UK Archbishop Ahead of G8 Summit

Tax avoidance is "sinful" and tantamount to robbery, says Archbishop John Sentamu, one of the UK's most senior clerics, as G8 leaders prepare to discuss the issue.

From the BBC:

From the BBC:

Dr John Sentamu, the Archbishop of York, told the BBC that individuals and companies needed to be held accountable for their actions when it came to tax.

Tax avoidance was hindering efforts to tackle hunger and malnutrition in developing countries, he suggested.

Business has urged politicians to focus on setting laws and not "moralising".

Tax avoidance was "definitely a moral issue", the archbishop said and asked whether it was sinful, he replied: "It is sinful, simply because Jesus was very clear; pay to Caesar what belongs to Caesar and to God what belongs to God."

Those not paying their full tax liabilities were "not only robbing the poor of what they could be getting, they are actually robbing God, because God says 'bring into my store house all the tithes'".

"So if God has told us to be just, to walk humbly and to be merciful and then we behave in a very strange way - God is being robbed, the world is being robbed, your neighbour is being robbed."

Business organisations have warned politicians against "moralising" about the issue and said it is the task of governments to set the laws regarding tax and for firms to abide by them. Google, Amazon and Thames Water all insist they are complying fully with the law.

Tuesday, June 11, 2013

So The Problem Is Not Just IRS Lawyers... It's All Government Lawyers?

There is a great article by Robert Anderson (Pepperdine) on how the IRS is just a microcosm of nearly all federal agencies. In a sense, the problem is not just IRS lawyers, but ALL government lawyers. He points out that 95% of IRS lawyers who contributed to last election's candidates contributed to President Obama--but surprisingly this lopsided giving is not out of the ordinary for government lawyers across nearly all agencies.

See below for relevant portions:

I searched the Federal Election Commission database for contributors with the term "lawyer" or "attorney" in thee occupation field. I then sorted the results by government agency (including the many permutations of agency names in the database). This produced a list of 20 federal agencies with at least 20 employees contributing to either Barack Obama or Mitt Romney in the 2012 election.(Hat Tip: Tax Prof Blog)

The results for the IRS were striking. Of the IRS lawyers who made contributions in the 2012 election, 95% contributed to Obama rather than to Romney. So among IRS lawyers, the ratio of Obama contributors to Romney contributors was not merely 4-to-1 at previously reported, but more like 20-to-1. The ratio of funds to Obama was even more lopsided, with about 32 times as much money going to Obama as to Romney from IRS lawyers.

So has the IRS gone off the rails into hyper-partisanship, leaving behind other more balanced federal agencies? ... The data show, however, that the partisanship of the lawyers in the IRS is not unusual or even particularly extreme among federal agencies. In fact, the lawyers in every single federal government agency--from the Department of Education [100%] to the Department of Defense [68%] -- contributed overwhelmingly to Obama compared to Romney. The table below shows the results for all agencies with at least 20 employees who contributed to either Obama or Romney. ...

Friday, June 7, 2013

The IRS Targeting Scandal--An Engaging Infographic

Below is a fascinating infographic that attempts to fill-in the details and give the back story of the IRS tea-party targeting scandal. (admittedly the tone is a bit left-leaning)

Source: TopAccountingDegrees.org

Source: TopAccountingDegrees.org

Wednesday, June 5, 2013

Am I Liable for my New Spouse's Old Tax Debts?

I get this question a lot from recent newly weds. Often, one of the spouses has racked up a massive tax bill and the "nonliable" spouse is worried that his or her assets will now be subject to IRS lien and levy procedures.

If you've just gotten married and your spouse's tax debts arose prior to marriage then you will have to work through a maze of California State and Federal rules to determine whether your assets can be attached by the IRS.

First, it is helpful to keep in mind that under federal law, the IRS (as a creditor) steps into the shows of the taxpayer and that state law determines a taxpayer's property rights to property. Because a federal tax lien against one spouse attaches to all of that taxpayer's property and rights to property in a community property state, the lien would attach to the liable spouse's one-half ownership interest in all items of community property.

In addition, in California, often times a private creditor has the right to collect a debt from all or part of both spouses' interests in community property. (See Fam. Code 910.) In other words, California is known as a 100% State, which means that the IRS (like other creditors) can collect from 100% of the community property for all the premarital tax debts of a spouse.

California does make a key exception to the nonliable spouse's wages that are earned after the marriage. As long as these wages are deposited into an account only in the nonliable spouse's name (and over which the liable spouse has no control or access and has not commingled funds), then these assets will not be subject to levy. (See Fam. Code 911.) However, if these funds are then used to purchase real property or vehicles, then such assets would then be subject to potential IRS lien and levy.

One way to protect additional community property assets would be to have the couple enter into a post-nuptial agreement whereby the spouse with tax issues would waive any community property interest in the other spouse's future earnings or property. Of course, this should only be done after careful consideration of all the relevant facts and circumstances and may be subject to challenge by the IRS as a fraudulent transfer.

If you've just gotten married and your spouse's tax debts arose prior to marriage then you will have to work through a maze of California State and Federal rules to determine whether your assets can be attached by the IRS.

First, it is helpful to keep in mind that under federal law, the IRS (as a creditor) steps into the shows of the taxpayer and that state law determines a taxpayer's property rights to property. Because a federal tax lien against one spouse attaches to all of that taxpayer's property and rights to property in a community property state, the lien would attach to the liable spouse's one-half ownership interest in all items of community property.

In addition, in California, often times a private creditor has the right to collect a debt from all or part of both spouses' interests in community property. (See Fam. Code 910.) In other words, California is known as a 100% State, which means that the IRS (like other creditors) can collect from 100% of the community property for all the premarital tax debts of a spouse.

California does make a key exception to the nonliable spouse's wages that are earned after the marriage. As long as these wages are deposited into an account only in the nonliable spouse's name (and over which the liable spouse has no control or access and has not commingled funds), then these assets will not be subject to levy. (See Fam. Code 911.) However, if these funds are then used to purchase real property or vehicles, then such assets would then be subject to potential IRS lien and levy.

One way to protect additional community property assets would be to have the couple enter into a post-nuptial agreement whereby the spouse with tax issues would waive any community property interest in the other spouse's future earnings or property. Of course, this should only be done after careful consideration of all the relevant facts and circumstances and may be subject to challenge by the IRS as a fraudulent transfer.

Sunday, June 2, 2013

IRS Scandal Extends to Gift Tax Return Abuse

Saturday's Wall Street Journal has a remarkable article disclosing that at the same time the IRS was subjecting tea-party groups to extra scrutiny, it also targeted tea-party donors by taking the unusual step of trying to impose gift taxes on donations to these groups.

In February 2010, the same month the tea-party targeting started, according to a recent inspector general's report, Freedom's Watch [a prominent conservative 501(c)(4)] was subjected to an IRS audit that focused largely on its political activities, an uncommon but not unprecedented action, election lawyers say. The probe broadened into other areas, including executive compensation.

About a year later, as many as five donors to Freedom's Watch were subjected to IRS audits of their contributions that sought to impose gift taxes on their donations to the group, according to lawyers and former officials of Freedom's Watch.

Believe it or not, the question of whether donations to tax-exempt groups like 501(c)(4)s are subject to the gift tax isn't necessarily settled law. The generally accepted protocol, however, was that if a donation was to a tax-exempt entity the IRS would not allege that gift taxes would apply.

Subscribe to:

Comments (Atom)